HMRC is now sending letters to thousands of young people in the UK, including those in North London, who may be owed money from old Child Trust Fund (CTF) accounts. These letters are part of a government‑wide effort to reunite people with forgotten tax‑free savings that could average around £2,200 per unclaimed account.

- What exactly are HMRC child trust funds letters?

- Why are HMRC sending these letters now?

- How do you know if an HMRC CTF letter is genuine?

- Who is eligible to receive an HMRC CTF letter?

- What information do HMRC CTF letters usually contain?

- How do you find your Child Trust Fund using HMRC?

- How do you access the money from a Child Trust Fund?

- What should North London residents do if they get a letter?

- What are the risks of ignoring HMRC CTF letters?

- Can you still claim if you never received an HMRC letter?

- How can North London residents protect themselves from scams?

- What happens to the money if you never claim it?

What exactly are HMRC child trust funds letters?

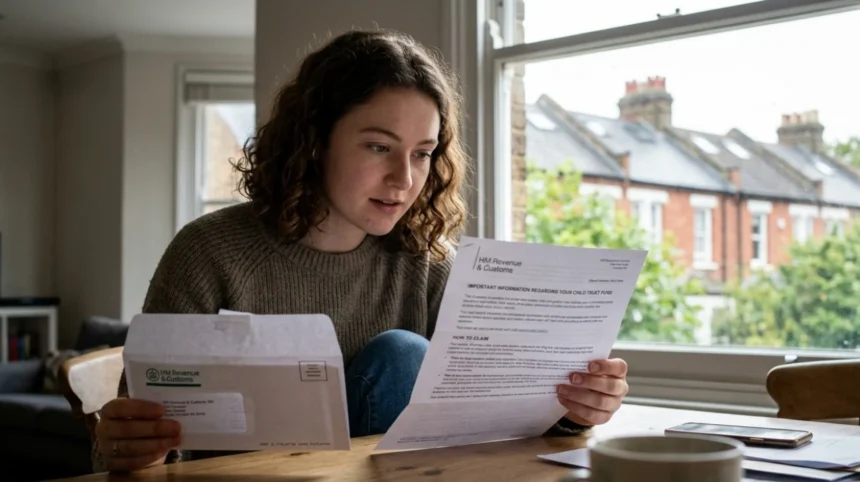

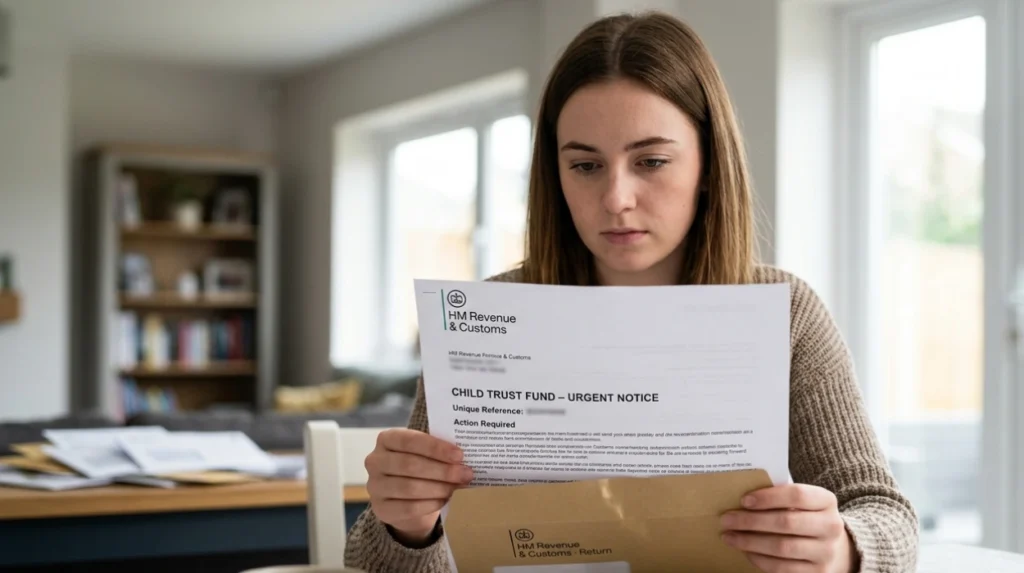

HMRC child trust funds letters are official notices sent by HM Revenue & Customs to inform people that they may have an unclaimed Child Trust Fund (CTF) account. These letters typically arrive around the recipient’s 21st birthday and include basic details about the account type, the provider that holds it, and instructions on how to contact that provider or apply for details through GOV.UK.

Child Trust Funds are long‑term, tax‑free savings accounts set up for children born between 1 September 2002 and 1 January 2011. Between roughly 2005 and 2011, HMRC paid an initial government contribution of £250 or £500 into most eligible accounts, depending on the family’s income and the child’s birth date. If parents did not choose a private provider within a set period, HMRC automatically opened a stakeholder‑type CTF on the child’s behalf.

The new letters are distinct from the original paperwork parents received years ago. Current HMRC CTF letters are reminder‑style communications, often triggered by national data‑matching campaigns. They are not welcome letters, thank‑you notes, or promotional mail; they are formal notices that an account exists and that the person is now eligible to access it.

Why are HMRC sending these letters now?

HMRC is sending these letters because an estimated £1.5 billion across roughly 750,000 CTF accounts remains unclaimed, even though around two‑thirds of the six million people who qualified for a CTF are now over 18 and entitled to their money. Many of these unclaimed accounts belong to young adults who moved house repeatedly, changed their names, or simply never kept track of paperwork from childhood.

The government has chosen 21 as the key age for this letter‑sending campaign because it assumes that most people have had some interaction with HMRC or tax‑related systems by then, such as applying for a National Insurance number or dealing with student‑loan or tax‑credit issues. HMRC can therefore use its existing address and contact data to reach a large proportion of eligible people.

Another reason for the timing is the closure of the CTF scheme itself. New CTFs stopped being opened after 3 January 2011, when the government replaced them with Junior ISAs. Because the scheme is closed, HMRC can now focus on settling outstanding accounts rather than managing new ones.

How do you know if an HMRC CTF letter is genuine?

A genuine HMRC child trust funds letter follows standard HMRC security and layout conventions. It will usually include the recipient’s full name, National Insurance number or a unique reference, and clear HMRC branding such as the GOV.UK logo and the words “HM Revenue & Customs” at the top of the page. The letter will also include a short explanation of what a Child Trust Fund is and why HMRC believes the person may have an account.

Genuine letters will not ask for sensitive information such as full bank account details, PINs, or passwords in the first contact. Instead, they will direct the recipient to use the official GOV.UK “Find a Child Trust Fund” service or to call an HMRC‑branded helpline number with a 0300 prefix. Any letter that demands immediate payment, threatens penalties, or demands card details via a provided link is very likely to be a scam.

If you are unsure, do not ring numbers printed on the letter straight away. Instead, enter “HMRC child trust fund” or “HMRC helpline” into GOV.UK and call the official contact number listed there. You can also mark suspected scam letters as “suspicious mail” through existing HMRC fraud‑reporting routes.

Who is eligible to receive an HMRC CTF letter?

HMRC CTF letters are sent to people who were born between 1 September 2002 and 1 January 2011 and who never claimed or accessed their Child Trust Fund before turning 18. They are targeted particularly at 21‑year‑olds, but older adults can still be eligible if their records are traceable and their account has not already been closed or withdrawn.

Eligibility is based on HMRC’s historical CTF records, which link to the original Child Benefit claim that triggered the CTF payment. If a parent or guardian received Child Benefit for a child in that date range, HMRC usually created a CTF or issued a voucher. The government estimates that around six million children qualified for a CTF, so the potential pool of letter recipients is large.

If a person has moved several times, changed their name, or never kept the original CTF paperwork, they may still be on HMRC’s list. HMRC matches its data against other government systems, including tax records and National Insurance registrations, to update addresses and contact details before sending letters.

What information do HMRC CTF letters usually contain?

HMRC child trust funds letters typically include the person’s name, National Insurance number or a case reference, and the child’s date of birth. They also state that the person may have an unclaimed Child Trust Fund and explain that HMRC can provide the name of the provider that currently holds the account.

The letter will normally outline two main options: apply online via the “Find a Child Trust Fund” service on GOV.UK or write to HMRC by post using the address and reference number printed on the letter. It may also note that if no response is received within a set period, HMRC may not be able to help further without additional information.

Importantly, these letters do not usually state the exact balance of the account. They are designed as “you may be owed money” prompts, not full account statements. To see the precise amount, the person must contact either HMRC to identify the provider or the provider directly once the account details are confirmed.

How do you find your Child Trust Fund using HMRC?

HMRC provides a dedicated “Find a Child Trust Fund” service on GOV.UK that allows a person to check whether they have an unclaimed CTF and obtain the provider’s details. The service requires the applicant to provide their name, date of birth, National Insurance number, and current address. HMRC then matches this information against its CTF records.

Once the request is submitted, HMRC typically sends a follow‑up letter within about three weeks for online applications, stating which provider holds the account. Postal applications can take longer, often up to six weeks. If HMRC cannot identify an account from the information given, it may ask for additional documentation or contact the applicant directly.

The process is free. HMRC does not require upfront payments or third‑party agents to trace a CTF. There are, however, commercial “claims firms” that offer to search for old accounts and charge fees of hundreds of pounds; these are unnecessary and can be avoided entirely by using the official GOV.UK service and contacting providers directly.

How do you access the money from a Child Trust Fund?

Once HMRC confirms which provider holds the CTF, the person must contact that provider directly to access the funds. Providers include banks, building societies, and insurance companies that specialised in long‑term savings products. The person will need to prove their identity, usually with documents such as a passport or driving licence and recent utility bills or bank statements.

If the account holder is over 18, they can generally withdraw the money without tax‑penalty. Child Trust Funds are tax‑free vehicles, so the balance and any built‑up interest are exempt from income tax and capital‑gains tax. Some providers may allow the money to be transferred into a standard savings account, a Junior ISA conversion (if the rules allow), or another investment product instead of a full cash‑out.

If the account has already matured or the provider has marked it as dormant, extra steps may be required. The provider may need to confirm residency status, update contact details on file, or process a dormant‑account release. These back‑end procedures are usually spelled out in the provider’s own guidance documents and can take several weeks from the time the request is submitted.

What should North London residents do if they get a letter?

North London residents who receive an HMRC child trust funds letter should treat it as a serious financial notice rather than junk mail. First, they should check that the letter looks genuine, using the HMRC style and wording guidelines outlined earlier. If the letter appears suspicious, they should report it through HMRC’s online fraud‑reporting channels and not engage with any phone numbers or links provided.

If the letter looks genuine, the next step is to act quickly. HMRC processing can be slower by phone or post, so using the online “Find a Child Trust Fund” service usually produces faster results. Residents should keep a copy of the letter, note down any reference numbers, and store digital photographs of the document in case they need to prove they received it.

Once the correct provider is identified, North London residents can either visit a local branch (if available) or complete the withdrawal process online. Many providers in London, including major banks and credit‑union‑linked schemes, support fully digital account‑handling for CTFs, so in‑person visits are not always necessary.

What are the risks of ignoring HMRC CTF letters?

Ignoring an HMRC child trust funds letter can result in several financial and practical risks. The most obvious is missing out on money that could be used for rent, deposits, or unexpected expenses; on average, unclaimed CTF balances are estimated to be around £2,200, which can be a significant amount for many young adults.

Another risk is that dormant‑account rules may lead to the account being transferred to a dormant‑account scheme or being subject to additional administrative checks. If the provider cannot contact the account holder, it may place the funds in a safeguarded pool, which can make later recovery more bureaucratic. In some cases, long‑dormant accounts may even be subject to local‑authority‑intervention rules, though this is rare for CTFs.

There is also a fraud risk. If someone ignores a legitimate HMRC letter and does not update their contact details, scammers may try to impersonate them and contact the provider. Keeping contact information up to date and acting promptly reduces the window of opportunity for identity‑theft‑linked fraud.

Can you still claim if you never received an HMRC letter?

Yes. A person can still claim a Child Trust Fund even if they never received an HMRC letter. The letters are part of a new outreach campaign, but they are not a legal requirement for claiming. HMRC’s underlying CTF records still exist, and individuals can trigger a search at any time by using the “Find a Child Trust Fund” service on GOV.UK.

If HMRC does not recognise the details an applicant provides, they may ask for additional evidence. This can include old CTF statement letters, proof of past Child Benefit claims, or documentation showing the child’s birth details and address history. North London residents with multiple address changes may find it helpful to compile a timeline of previous addresses and landlords to support their request.

Even if the original CTF paperwork was lost, HMRC can often reconstruct the record using its internal databases. The key is to provide as much accurate information as possible and to keep records of every step taken, including confirmation emails from GOV.UK and any letters from providers.

How can North London residents protect themselves from scams?

North London residents can protect themselves from scams by treating all unsolicited financial messages with caution. If a text, email, or social‑media message claims to be about a Child Trust Fund and includes a link or phone number, it should be verified against the official GOV.UK contact details before any action is taken.

Residents should never share full bank‑account details, PINs, or full card numbers in response to a letter, email, or website that is not clearly linked to HMRC or an authorised provider. Genuine HMRC communications will not ask for this level of information upfront. If a letter or website insists that a fee must be paid to “release” CTF funds, that is a strong sign of a scam.

It is also wise to inform family members or carers about CTF‑related scams. In North London’s diverse communities, where some households may have limited English or digital literacy, a simple explanation that “no‑fee rules apply” and “always check GOV.UK first” can prevent people from paying unnecessary third‑party charges.

What happens to the money if you never claim it?

If a Child Trust Fund is never claimed, the money remains held by the provider or, if the account is dormant, by a designated dormant‑account scheme. Providers cannot spend or invest the money for their own benefit; they are legally required to protect the balance and to allow the account holder to reclaim it at any time, even decades later.

In some cases, if the provider changes hands through mergers or acquisitions, the account may be transferred to a successor institution. Original providers such as certain building societies or insurance companies may have been bought by larger banks, but the underlying CTF balance is still traceable through HMRC’s records and the provider’s archive systems.

Long‑term inactivity can sometimes lead to administrative costs being deducted from the account, depending on the specific product terms. However, these deductions are usually small and clearly outlined in the provider’s terms and conditions. The core principle is that the money remains the account holder’s property, even if it is not actively accessed.

What is an HMRC Child Trust Fund letter?

An HMRC Child Trust Fund letter is an official notice from HM Revenue & Customs informing you that you may have an unclaimed Child Trust Fund (CTF) account. It usually explains how to trace the account and contact the provider.